Europe’s Discount Opportunity: Why Global Capital Is Quietly Returning to Eurozone Assets

March 25, 2026

For over a decade, since the GFC of 2008, the investment narrative for global hedge funds and managers has been rather straightforward – look to the US where growth was happening at high decibel, where tech innovation was shaping the structure of the global societies, look at China which was standing head-to-head with the US in all sectors including global expansion, move to the rest of Asia – Japan, Ems et al, where, due to a lower base, growth was headlined by huge markets. Europe, and the eurozone, was often seen as a laggard, with muted growth, caught in cycles of energy crises, ageing demographics, and fragmented policy initiatives.

Not any longer. For the prescient investment manager, the Eurozone is no longer an anathema. There is a quiet but visible change that is sweeping across continent that is shaping up to attract global capital – not because the rest of the world, including the US is performing badly, but primarily because there appears to be a structural change in the Eurozone that may be combining, growth resilience and newer structures of investment that may well make it a strategic necessity.

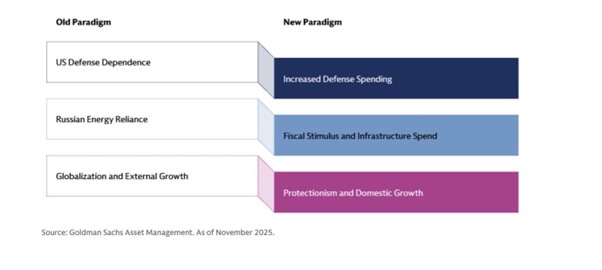

According to Goldman Sachs, there is a paradigm shift underway in Europe1 wherein the erstwhile pillars of growth, which were largely driven by external factors, are being replaced by newer pillars that are more internally driven and predicated by the EU’s own strategic necessities.

Source: Goldman Sachs2

Valuation Gaps and Earnings Growth

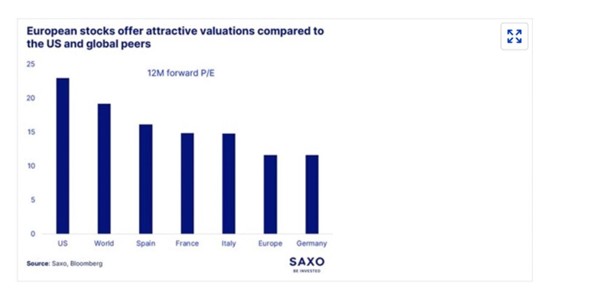

At the heart of this rebound is the significant valuation gaps that have emerged between the US and the EU. According to research, European equities currently trade at significant valuation discounts relative to the US, with forward price-to-earnings (P/E) multiples around 12x, compared to approximately 23x in the US. Europe’s average dividend yield is near 3.3%, substantially exceeding the US average of about 1.3%.3

Source: Saxo4

This is not just a bargain but provides a margin of safety. According to the Vanguard’s ‘Great rotation’ published recently, while the US stocks get rattled by even a minor deviation from expectations, perhaps due to the “stretched” valuations, European stocks have priced in the “guardedness,” making them resilient to macro shocks.5 The valuation gap narrative would be moot without an underlying growth narrative. According to JP Morgan estimates, earnings projections for 2026 are much higher at nearly 15% on a combination of easy base effects, an improving macro backdrop, rising liquidity, a better China outlook, and fiscal stimulus.6

The gap between US and European earnings growth, which averaged 8 percentage points annually since the global financial crisis, is expected to shrink to 2 percentage points between 2025 and 2027. Investors can thus pay a multiple of 16x forward earnings in Europe (ex-UK), compared to 23x in the US, for relatively similar future earnings streams. That is a compelling proposition for long-duration capital.

Industrial Policy as a Structural Catalyst

Beyond the cyclical recovery, Europe is undergoing a genuine industrial policy renaissance.

Former ECB head Mario Draghi outlined three priority areas to restore sustainable growth momentum in Europe: closing the innovation gap with global leaders, reducing energy costs while continuing the transition to clean energy, and strengthening economic security and resilience, including building a more robust defence-industrial base and reducing strategic dependencies in key areas such as critical raw materials and digital infrastructure.7

While the Draghi report has yet to be fully implemented, there has been significant movement across several sectors.8 In February 2025, the EU launched InvestAI, a €200 billion initiative covering AI, cloud infrastructure, semiconductors, and data centres. Germany’s government set up a debt-financed special fund of €500 billion for infrastructure over 12 years, while REPowerEU has mobilised €325 billion for energy efficiency and securing critical raw materials.

These are not timid incremental measures. They represent a deliberate effort to close the productivity gap with the United States that Draghi identified in his landmark 2024 report.9 Progress on these structural reforms could underpin growth further, and that is an opportunity as much as a concern.

Capital Repatriation: A Structural Shift Underway

Perhaps the most underappreciated driver of the Europe story is capital repatriation. Draghi’s report calls for around €800 billion in investment, of which the majority (around €650 billion) will come from the private sector.10 As a result, Europe’s roughly €300 billion annual savings surplus needs to be actively incentivised, through taxation and regulation, to be invested in Europe rather than abroad.

Geopolitical uncertainty is accelerating this calculus. As confidence in the predictability of US policy has wavered, institutional investors are revisiting their asset allocation frameworks. LP surveys from Preqin, reported by GIIA, indicate a planned 5-7% increase in EU allocations by 2026,11 largely funded by trimming US exposure, while mature European regulated asset stakes trade at a 6–8% premium to net asset value.

The Rise of the “Industrial Accelerator”

Europe is currently undergoing its most significant policy shift since the creation of the Single Market. The transition from the “Green Deal” to the Clean Industrial Deal and the newly proposed Industrial Accelerator Act (March 2026) marks a pivot toward “strategic autonomy.”12

Unlike previous eras of open, non-discriminatory procurement, Brussels is now explicitly favouring “Made in EU” production for strategic sectors like:

- Green Tech: Batteries, EVs, and hydrogen electrolyzers.

- Defense: A sector that, while historically small, is seeing massive execution pick-up and multi-year budget commitments across the bloc.

- Energy-Intensive Materials: New quotas for low-carbon steel and aluminium are creating a “green premium” for European manufacturers who have already invested in decarbonization.

This “mission-oriented” policy is acting as a massive de-risking mechanism for private capital. When the state provides streamlined permitting and guaranteed demand through public procurement, infrastructure and private equity funds follow.

It is Not Exuberance But Structural

The case for Eurozone assets is not built on exuberance; it is built on relative value, structural policy shifts, and evolving capital flows.

For global investors, Europe represents a valuation-driven reallocation opportunity with additional plays on a new industrial superstructure with a hedge against over-concentration in the US markets. The narrative is shifting, slowly but surely, from Europe as a laggard to Europe as a strategically undervalued component of global portfolios.

Sources:

2. https://www.jpmorgan.com/insights/global-research/markets/european-stocks

4. https://viewpoint.bnpparibas-am.com/private-capital-in-europe-a-e3-trillion-investment-super-cycle/