The Return of the Risk-Mitigator: Why Pensions Are Re-Allocating to Hedge Funds in 2026

April 28, 2026

Remember September 2014, when CalPERS, the largest pension fund in the US, famously announced its withdrawal from hedge funds? While the fund officially stated that the decision was not due to modest returns, at the time, it was reported that CalPERS’ decision was influenced by weak returns and exacerbated by high fees and a lack of transparency. Cut to 2025. The $600 billion fund has spent 2025 and early 2026 quietly but firmly rebuilding its “opportunistic” and risk-mitigation buckets.

Recent reports1 show CalPERS has committed billions to niche, uncorrelated strategies. This includes a massive push into Insurance-Linked Securities (ILS) and catastrophe bonds, totaling over $1.45 billion by the start of 2026, as well as private credit mandates that function as portable alpha vehicles. By utilizing Separately Managed Accounts (SMAs), CalPERS and its peers now have more control over fees and transparency than they did a decade ago.

So What Gives?

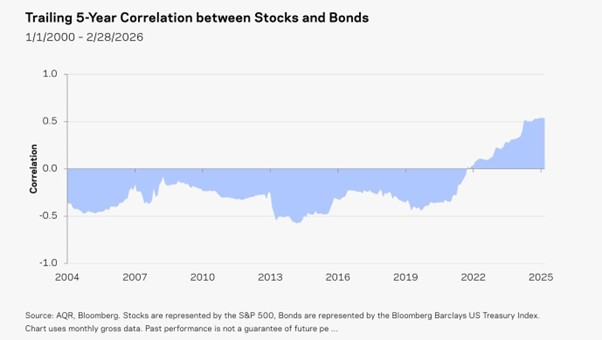

The primary driver for this shift is a fundamental breakdown in traditional diversification. Historically, when stocks fell, bonds rose. However, in a post-COVID world, the positive correlation between stocks and bonds, largely driven by sticky inflation and shifting central bank policies, has rendered the classic 60/40 portfolio insufficient.

Source: AQR2

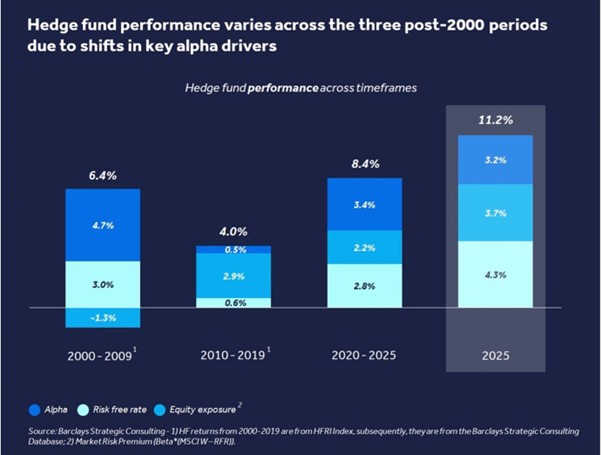

The Rise of Non-Directional Sleeves

In 2026, institutional allocators are returning to hedge funds not out of nostalgia, but out of necessity. The dominant question is no longer how do we capture more upside? It is how do we protect what we have?

The objective is resilience in a world where volatility has become boring. Geopolitical fragmentation, sticky inflation, active central bank policy, and the tariff-driven uncertainty of 2025–26 have created a market landscape in which investors are seeking funds that can deliver returns uncorrelated with market beta.

Source: Barclays Investment Bank3

According to a Hedgeweek report4, a Goldman Sachs survey of pension funds, family offices, funds of funds, and other major allocators revealed that 49% of respondents plan to increase hedge fund exposure in 2026 – up sharply from 37% just a year earlier. Only 4% intend to reduce. The resulting net figure of +45% planning to add exposure is the highest recorded in Goldman’s survey data since 2017.

This isn’t just sentiment. Capital is moving. Hedge funds recorded5an estimated $79 billion in net inflows in 2025 — the first annual inflows in several years — and Goldman Sachs expects flows to improve further in 2026. The industry is now on track to hit $5 trillion in AUM a full year ahead of schedule, by 2027 rather than 2028.

The language has changed. Allocators are no longer talking about hedge funds primarily as return enhancers. They are talking about building non-directional sleeves: dedicated allocations to strategies explicitly designed to generate returns uncorrelated with broader market beta. The goal is portfolio resilience, not outperformance in a bull market.

According to With Intelligence’s 2026 Hedge Fund Outlook, “large institutions [are] continuing multiyear programs to build out sizeable non-directional sleeves.”6 This is a structural, deliberate architectural choice — not a tactical tilt. Barclays Investment Bank’s 2026 Hedge Fund Outlook confirms this structural preference: investors are showing “a growing preference for higher volatility strategies and lower beta exposure,” and are “increasingly favouring managers who can deliver uncorrelated returns regardless of market environment.”7

Key Strategies in the Sleeve:

- Quantitative Multi-Strategy: Using AI-driven algorithms to capture micro-inefficiencies.

- Discretionary Macro: Betting on the divergence of global economies and central bank policies.

- Equity Market Neutral: Hedging out market risk to capture pure alpha (manager skill).

The trends are evident at both the supply and demand sides. Pension funds are actively considering reallocating to hedge funds while insisting on greater transparency. For instance, in early 2026, the Teachers’ Retirement System of Illinois (TRS) approved nearly $1 billion in new commitments to hedge funds and private market strategies to enhance returns while reducing portfolio volatility. Others, like Texas Teachers and Norway’s Norges Fund, are also reportedly actively considering significant investments in hedge funds and other alternatives.

In plain English: different parts of the world are moving in different directions at different speeds. For a pension fund invested in the market, this is a headache. For a hedge fund manager, this is an opportunity to profit from the price dislocations between those regions.

The macro environment of 2026 is a playground for hedge funds. While 2025 saw a Goldilocks rally, 2026 began with what BlackRock describes as a “fragile market equilibrium.”8 The divergence between the Federal Reserve’s duration management and the European Central Bank’s balance sheet tightening has created cross-country dispersion.

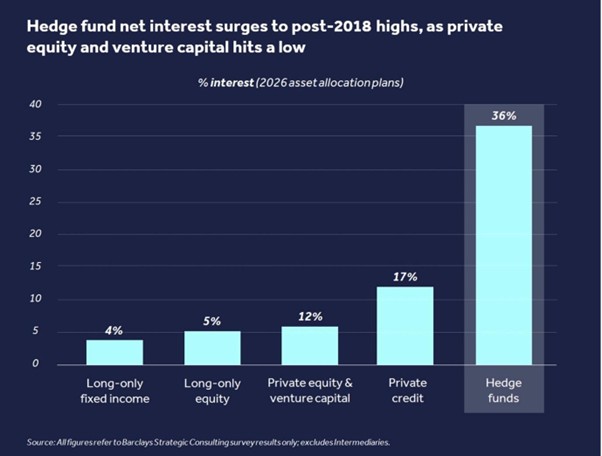

Liquidity: The Hidden Driver

Another reason pensions are pivoting back to hedge funds is the liquidity trap of private markets. For years, pensions over-allocated to Private Equity (PE). Now, with slower distributions and dry powder reaching record levels, many funds are finding themselves over-allocated to illiquid assets.

Hedge funds offer a middle ground: better returns than cash or standard bonds, but with significantly more liquidity than a 10-year PE fund. Barclays Investment Bank notes that sentiment toward hedge funds is at its highest level since 2018, driven by investors “repositioning in search of liquidity and performance”9 away from stagnant private equity holdings.

Source: Barclays Investment Bank10

A New Mandate

The 2026 hedge fund allocation is not about beating the S&P 500. It is about portfolio insurance. Pensions are no longer asking hedge funds to be their growth engine; they are asking them to be the anchor. As volatility remains the only constant in the 2026 global economy, the return of the Risk-Mitigator suggests that the most valuable asset in a pension’s portfolio isn’t the one that grows the fastest—it’s the one that stays steady when everything else is shaking.

Sources:

3. https://www.ib.barclays/our-insights/3-point-perspective/hedge-fund-outlook-2026.html

4. https://www.hedgeweek.com/hedge-funds-carry-momentum-into-2026-after-beating-expectations-in-2025/

5. https://www.withintelligence.com/insights/hedge-fund-outlook-2026/

6. Ibid.

7. https://www.ib.barclays/our-insights/3-point-perspective/hedge-fund-outlook-2026.html

9. https://www.ib.barclays/our-insights/3-point-perspective/hedge-fund-outlook-2026.html

10. Ibid.