The Divergence Play: What Happens to Global Markets When the BOJ Hikes and the Fed Holds?

May 31, 2026

The global macroeconomic landscape is witnessing a classic policy divergence. Since the pandemic, the global financial system has operated under a predictable rhythm: the Federal Reserve has led the world’s monetary policy dance, while the Bank of Japan (BOJ) has remained anchored to ultra-loose, near-zero (or negative) interest rates.

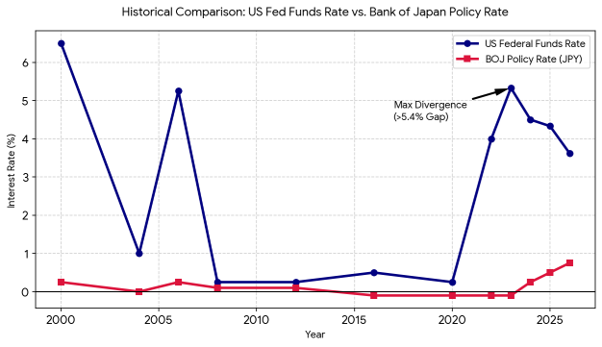

The script appears to be flipping. The global monetary policy landscape is approaching a historic inflection point. The Bank of Japan (BOJ) is increasingly likely to raise interest rates at its June meeting, with 65% of economists forecasting a move to 1.0% by the end of June.1 Meanwhile, the Federal Reserve is expected to hold rates steady at approximately 3.75%, having paused its cutting cycle.2As the Fed adopts a firm “wait-and-see” posture—holding rates steady at 3.5%-3.75% amid sticky inflation and geopolitical tensions—the BOJ is moving in the opposite direction. Facing persistent domestic price pressures, Tokyo policymakers are signaling further interest rate hikes, pushing their benchmark closer to the 1.0% mark.

To understand how this macroeconomic shift will impact global capital, we must examine these central bank decisions both in isolation and as a powerful, interconnected tandem.

The Fed Hold: Defending the Higher-for-Longer Plateau

Standing pat is a deliberate, defensive strategy for the Federal Reserve. By maintaining a restrictive benchmark rate, the Fed is attempting to cool resilient consumer price inflation without triggering a severe labor market contraction. Seen in isolation, a Fed hold keeps U.S. Treasury yields elevated and preserves the inherent appeal of the U.S. dollar. For domestic markets, it acts as a ceiling on equity valuations, keeping borrowing costs high for corporations and home buyers and credit conditions tight.

The BOJ Hike: Dismantling the Era of Cheap Cash

No matter how you look at it, the BOJ’s transition toward normalization is monumental. Since Sept 2001, JPY interest rates have hovered around 0.3% to near-zero, except for a brief 27-month period during the 2006-08 financial crisis, when they crept up to 0.75% before falling back to 0.3% until Dec ’24. Effectively, for the last two decades, Japan was the world’s premier exporter of capital, driven by domestic yields so low that keeping cash at home made little economic sense. At a national level, it made sense. For decades, the BOJ fought deflation, weak wage growth, and stagnant domestic demand. Negative rates and yield-curve control became permanent fixtures of the financial landscape.

However, since August 2024, the era of cheap cash has begun to fade. Japan is now experiencing something it has not consistently seen in years: sustained wage growth, firmer inflation, and a growing belief that domestic demand may finally support normalization. Tightening monetary policy is designed to defend the battered Japanese Yen (JPY) and stabilize domestic purchasing power. By raising borrowing costs, the BOJ incentivizes domestic institutions and retail investors to keep their money in Japan, pushing up Japanese Government Bond (JGB) yields and fundamentally shifting local asset pricing.

The Tandem Effect and Global Macro Mechanics

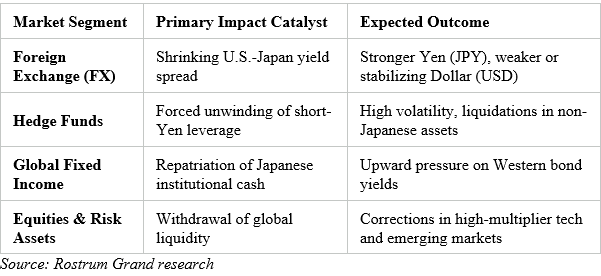

When you combine a rising Japanese rate with a flat U.S. rate, the structural plumbing of international finance begins to shift. The narrow gap between U.S. and Japanese yields triggers a massive unwinding of the financial mechanism known as the Yen Carry Trade. Such unwinds are rarely orderly. A sharp appreciation in the yen forces leveraged investors to deleverage positions globally, creating volatility across equities, bonds, and commodities. With the BOJ hiking and the Fed holding, this yield differential shrinks. The carry trade becomes less profitable and exponentially riskier, forcing a rapid, global repatriation of capital back into Japan.

The ripple effects of this cross-border monetary tug-of-war will vibrate across several distinct layers of the global financial system.

- Hedge Funds and Alternative Managers

Hedge funds are squarely in the blast zone. Many macro funds have long held structural short positions on the Yen while leveraging long positions in U.S. mega-cap equities or high-yielding emerging market debt.

As the Yen strengthens rapidly due to the BOJ’s hawkishness, these short positions face a squeeze. To cover their rising Yen liabilities, hedge funds will be forced to sell off their most liquid global winners. This forced deleveraging can trigger sudden, localized flashes of volatility across international equity and crypto markets.

- Broad Global Financial Markets

The shift in Japanese institutional behavior alters global liquidity flows:

-

- Fixed Income: Japanese lifers and pension funds are among the largest foreign holders of U.S. Treasuries and European bonds. As domestic JGB yields become attractive, these massive entities will reduce their foreign bond buying and bring cash home. Lower foreign demand for U.S. debt may put upward pressure on Western yields, even with the Fed on hold.

- Equities: Global equity markets will lose a key source of cheap liquidity. The historical correlation shows that a rapidly strengthening Yen often acts as a headwind for global stock indices, as global capital conditions tighten.

- Emerging Markets (EMs): Emerging economies are caught in a crosscurrent. On one hand, a cooling U.S. dollar offers relief to countries holding dollar-denominated debt. On the other hand, EMs that relied on cheap Yen inflows to fund their growth may experience sudden capital flight as investors pull back to safer, higher-yielding Japanese domestic assets.

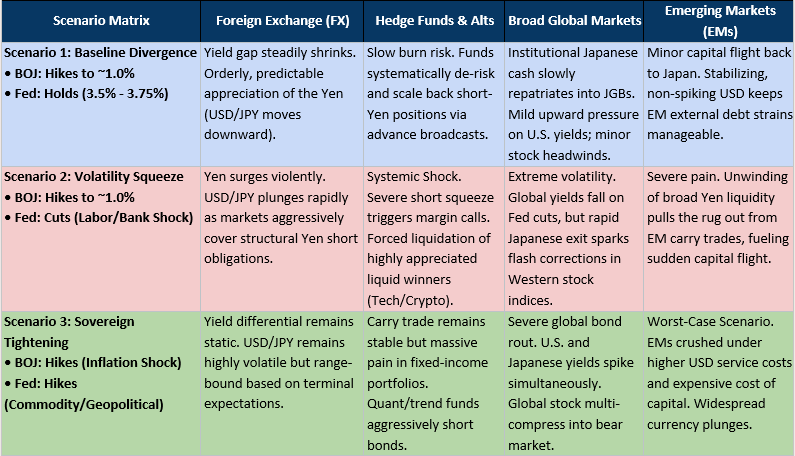

Scenario Mapping

When evaluating a Bank of Japan (BOJ) rate hike, the macroeconomic outcome depends heavily on what the Federal Reserve is doing simultaneously. Because the U.S. Dollar-Japanese Yen (USD/JPY) currency pair is the bedrock of global liquidity pricing, changes in the interest rate differential between these two superpowers alter how capital flows worldwide.

The three distinct scenarios below outline the market impact when the BOJ hikes rates to approximately 1.0% while the Fed holds rates, cuts rates, or hikes rates

Is this the Endgame?

Possibly not. There are already signs of strain within the US financial system, including the Fed, which is calling for a cut in interest rates. On the other hand, the ongoing conflict in the Gulf region has folks backing a rate hike. Given the current fluid situation, it is difficult to predict which way the Fed decision will swing.

Having said that, the synchronized reality of a hawkish Bank of Japan and a paused Federal Reserve signals the end of an era for frictionless macro trades. As the yield gap narrows, the global financial system must adjust to a world in which Japanese capital is no longer practically free, and U.S. capital remains stubbornly expensive. For investors, navigating this policy divergence will require shedding old assumptions about liquidity and preparing for a more volatile, fragmented global marketplace.

Sources:

2. https://tradingeconomics.com/united-states/interest-rate/news/546167