Evolving with the times: The distressed debt investing playbook

February 28, 2022

Vulture investors. Scavengers. And quite a few more colorful sobriquets. The world knows distressed debt and credit investors by different names. But ask any of them, and they will just shrug off these characterizations of theirs, and chug along, doing what they do best – being the “canary in the coal mine”.

Ever since distressed investing emerged as a mainstream asset class around 40 years ago, practitioners of this niche, specialized skill set have, and continue to, perform a critical function in global financial markets – signalling inefficiencies in the pricing of securities across the credit and fixed income spectrum.

And this class of investors has done so by typically mounting opportunistic wagers on defaulted or near-default bonds, making rescue loans, or even swooping for troubled borrowers via bankruptcy protection proceedings.

Continuous evolution

Back in the late 1980s, the distressed credit market was largely focused around U.S. “junk” bonds, before getting diversified to include bank debt, residential real estate loans, and under-priced non-U.S. securities.

The 1990s saw distressed investors lap up complex, yet opportunistic, situations, particularly in illiquid market segments or niche industries where companies were struggling to access capital.

The gradual evolution of distressed investing continued in the previous decade, in the aftermath of the 2008-09 Global Financial Crisis (GFC), thanks to a large-scale retrenchment by banks from the credit landscape amid imposition of tougher capital requirements and curbs on proprietary trading. Over the last 12 years, many hedge funds and private equity firms morphed into providers of direct lending and structured credit, beside acquiring non-performing bank loans, etc.

Essentially, the world of distressed investing has dynamically evolved over different market cycles in recent decades, wherein traditional distressed debt’s core, underlying investing thesis of robust downside protection and dramatic upside potential has been applied successfully to new, emerging market pockets like private credit.

The post-GFC economic expansion in the U.S., the longest in the country’s history, ran for 128 months, thereby helping many “zombie” companies, those with high debt-to-earnings ratios, stay afloat and reducing credit defaults significantly. The protracted recovery, enabled in no small measure by unprecedented levels of accommodative and unconventional central bank policies, saw a decline in credit risks, narrowing of credit spreads, and an overall improvement in corporate fundamentals.

This dynamic has substantially reduced the consideration set for distressed investors in recent years, in terms of them finding attractive opportunities to put their capital at work.

Post-COVID trends

The Federal Reserve’s ultra-aggressive monetary stimulus measures, announced in the wake of the COVID pandemic in March 2020, has further made the investing landscape challenging for distressed credit and debt funds.

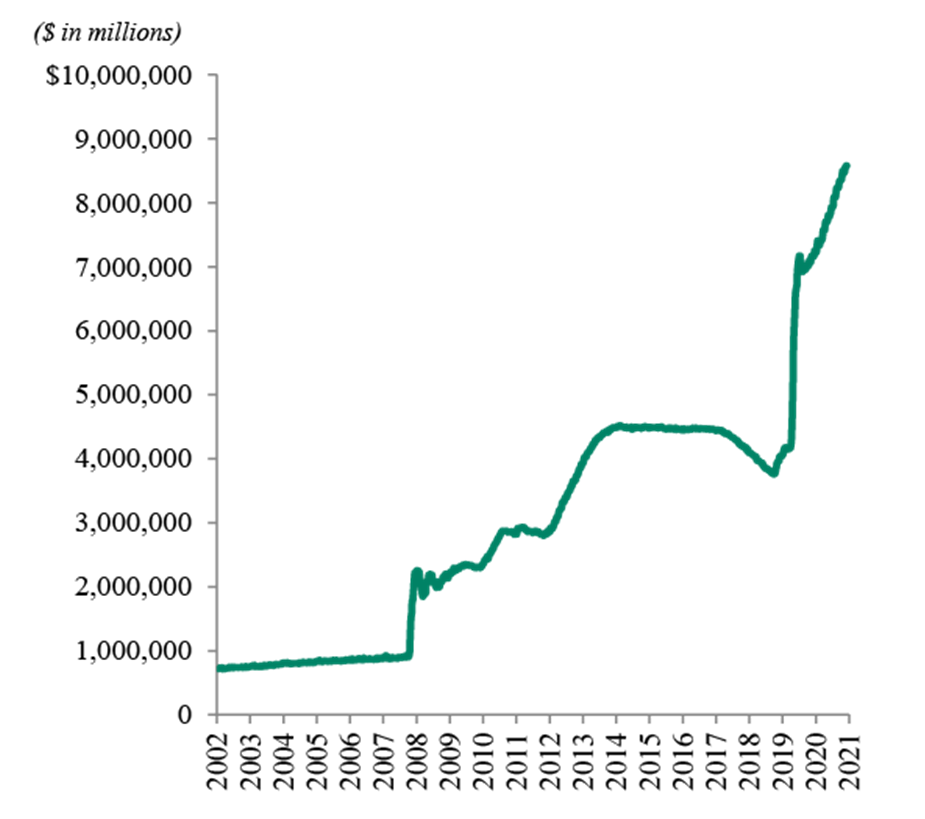

With the U.S. central bank expanding its already bloated balance sheet (see chart below) by almost $2 trillion in a matter of weeks then, to over $8.5 trillion, the unprecedented provisioning of liquidity across the board ensured that the double-digit default rates predicted by credit ratings agencies in early 2020 never came to fruition.

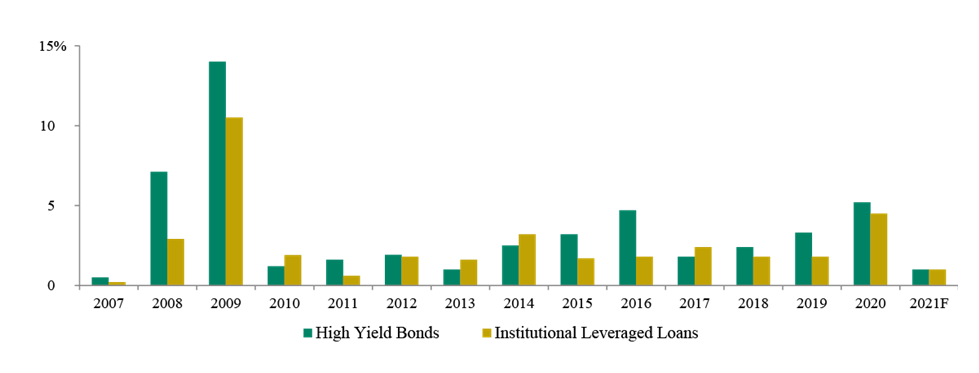

In fact, the multi-year economic expansion and monetary stimulus have artificially suppressed the levels of corporate defaults and bankruptcies, with debt default rates currently at 1%1 per annum, as compared with historical levels of 5%.

That has prompted several leading distressed investors to adapt their playbook for the new market environment.

Beside looking to snap up discounted corporate loans and bonds, many players in this space have taken to so-called rescue financing, providing credit to companies in troubled industries like aviation, event management and real estate that are shunned by banks and other capital providers.

Other distressed investors have also started rolling out credit to businesses seeking to strengthen their balance sheets and make capital expenditures, amid rising consumer demand.

Conclusion

Distressed credit has, and will continue, to play an anchor role in financial markets, irrespective of the nature of the investing cycle. As raging inflation in developed economies is likely to force the hand of central banks to tighten monetary policy and pull back liquidity, the long-awaited normalization and repricing of several debt and loans – including in the high-yield market – could finally occur, thereby placing distressed investment funds back in the spotlight.

Moreover, industry- and company-centric dislocations will keep recurring irrespective of the state of the broader market and default rates, presenting specialized investors with an opportunity to deliver true alpha for their clients.