From Capacity to Craft: Can Smaller, Niche Hedge Funds Outperform Mega Platforms, and Why?

February 23, 2026

Let us start with a disclaimer. Large hedge funds provide stable returns, offer multiple levels of derisking, have abundant tech skills, and have a bevy of managers tasked with ensuring that all signals are captured. Most Multi-strategy platforms can diversify across dozens of independent teams, reducing volatility and delivering more consistent returns.

But, herein lies the kicker. Information is the new holy grail, and a specialised manager with an intimate understanding of the sector in question will likely be able to move faster without worrying about layers of management controls and generate alpha. Most smaller funds have fewer layers of management, a far higher level of manager capability, and, most importantly, greater agility in decision-making.

This is not to knock the mega funds. For decades, they have provided stable, scalable returns and have armed themselves with much-envied pools of talent and technology to ensure that the vast sums of money they manage have built-in mechanisms to first protect wealth and secondly identify opportunities to optimise returns.

However, their very size could be an inhibitor. Mega platforms often manage so much capital that they become “the market.” If a $50 billion fund wants to take a position in a mid-cap stock, its sheer size can move the price before the trade is even completed-a phenomenon known as market impact. This ‘diseconomies of scale’ limits larger funds to “mega-cap” stocks or highly liquid macro instruments, effectively shrinking their investable universe.

In contrast, smaller funds can play in “unregulated” or neglected corners of the market, such as micro-cap equities, distressed debt in emerging markets, or exotic derivatives, where the “alpha” hasn’t been traded away by thousands of algorithms.

There is another systemic issue. Mega platforms often use similar quantitative models. When a “risk-off” event occurs, these giants often exit their positions simultaneously, creating “crowded trades” that can collapse rapidly. Smaller, niche funds often hold idiosyncratic positions that are uncorrelated to these massive flows. The recent ‘Saascalypse’1 in AI stocks due to Anthropic’s announcement of a legal solution is a case in point. The announcement led to a crowded trade that significantly drove down select stocks worldwide for 3 days.

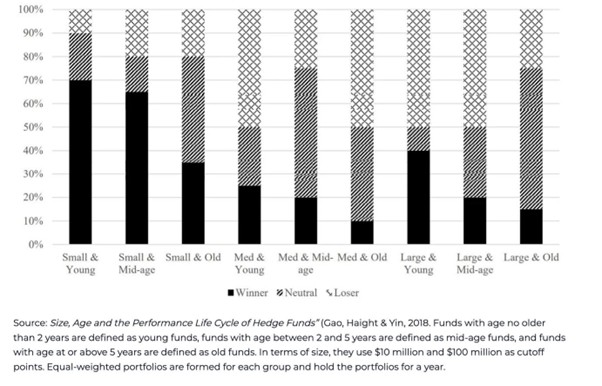

There is enough evidence to suggest that smaller, nimbler firms can generate higher returns than the Mega funds. In fact, a study conducted in 2018 shows that smaller funds-especially those under $500 million-tend to outperform their larger peers on a risk-adjusted basis. This is especially true in capacity-constrained strategies, where alpha degrades as AUM scales.

Source: Resonanz Capital2

The primary reasons for the above are:

- A smaller fund can be highly selective in comparison to a mega fund, which has capacity limits

- Larger firms, by their sheer size, can move markets, thus eroding Alpha. A smaller fund can actually identify opportunities (the signals) and move faster, so it can tap them immediately without causing a market impact.

- As clients start balking at the management fees that they need to pay, the smaller fund can be extremely flexible and trade off between management fee and performance incentives, something that a larger fund may be unable to do structurally.

- Finally, the manager in a mega-fund is, at the end of the day, an employee sitting in rigid structures. On the other hand, a smaller fund has the freedom to create structures that may be more inclusive and offer the manager much more upside potential, with corresponding downside risk.

Specialization and Informational Edge

Niche hedge funds often focus on narrow domains, such as semiconductor supply chains, healthcare royalties, distressed credit, or regional markets. This specialization allows managers to develop deep informational advantages that large, diversified platforms cannot easily replicate.

Informational edge is central to alpha generation. By conducting proprietary research, building industry relationships, and understanding complex market structures, specialized managers can identify opportunities invisible to generalist investors.

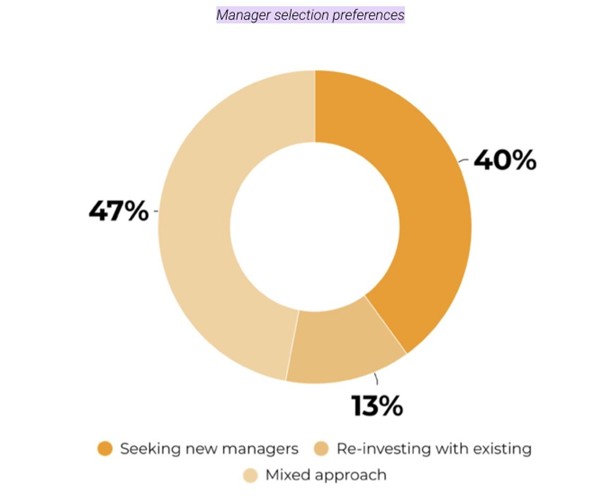

A Hedgeweek survey3 reveals that performance pedigree, long considered the top factor for allocators, is giving way to operational excellence, with most allocators giving operational due diligence a much higher weightage than in previous periods. The survey also reveals that 40% of allocators are seeking newer relationships over existing ones. This is an important signal for the smaller funds, as one area where they could score over the mega-funds is operational excellence and due diligence.

Source: Hedgeweek4

Large multi-strategy platforms, while possessing significant resources, often emphasize risk management and diversification over deep specialization. Their structure prioritizes stability and scalability, which can dilute individual strategy edge.

Craft Versus Capacity

Ultimately, the distinction between large and small hedge funds reflects a broader tension between capacity and craft. Mega funds excel at delivering stable, scalable returns through diversification, risk management, and infrastructure. Smaller funds excel at generating alpha through agility, specialization, and informational edge.

In an increasingly efficient and competitive market environment, true alpha may become even more constrained by capacity. As mega platforms absorb larger pools of capital, smaller niche managers may remain uniquely positioned to exploit inefficiencies inaccessible to larger competitors.

For allocators, the implication is clear. Mega hedge funds provide stability. But smaller, specialized hedge funds may provide something far more valuable: genuine alpha. And one more thing: alpha does not scale linearly with capital.

Sources:

4.Ibid.