Hedge Funds and the Rise of Sovereign Industrial Policy

June 22, 2026

How Smart Money Is Repositioning Around Government-Led Industrial Strategies

The more-than-75-year-old economic thesis is undergoing a profound change. Ever since the end of WW2, the largest economy in the world — the US — operated under capitalism, defined by minimal government intervention in the economy, except for policies and oversight; the private corporate sector was the chief producer, and markets were characterized by efficiency. For the most part, the hedge funds followed this narrative, defined by globalization, open capital flows, and the efficiency theme.

However, recent geopolitical conflicts and the emergence of technology as a tool of trade leverage have redefined this theme. In the last few years, a new world order is emerging- one defined by nationalistic economic postures, weaponization of resources, and, consequently, deliberate deployment of the government and its capital to economic sovereignty. The political establishment, which was considered to be more noise, has suddenly become one of the chief creators of the signal. State-led industrial strategy, once looked down upon, has now become the new alpha generator. Sophisticated investors are not fighting this tide. They are riding it.

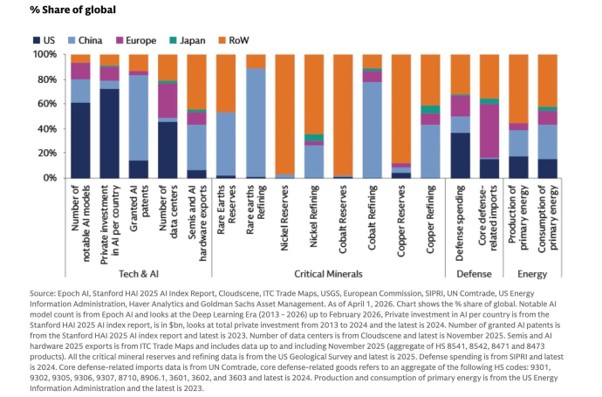

At a fundamental level, the ‘new regime’ narrative runs across four major vectors – Technology, Critical Minerals, Defense, and Energy as major investible themes with sub-themes in each of the vectors. According to a Goldman Sachs report, globally, while the US has a massive lead in Technology and AI, China and the rest of the world have an edge in critical minerals, with defense and energy much more dispersed.1

Source: Goldman Sachs Asset Management2

The New Regime: Industrial Policy as Investment Signal

If one were to trace the origins of the ‘New Regime’, one could argue that the shift began in earnest with the U.S. CHIPS and Science Act, which dedicated $39 billion to incentivize domestic semiconductor manufacturing. The results have been striking: by late 2025, the Semiconductor Industry Association reported that since 2020, CHIPS-linked activity had catalyzed more than $640 billion in investment across 140 projects, creating 500,000 jobs in 28 states.3 From a hedge fund perspective, this is more than just industrial policy — it is a structured, multi-year pipeline of investable opportunities that hedge funds with the right positioning can access.

In the policy realm, more direct action was to come. In 2025, the U.S. government began taking direct equity stakes in strategic companies, a remarkable departure from tradition. The administration used the Commerce Department’s “other transaction authority” to acquire a 10% stake in Intel through an $8.9 billion common stock investment, and in May 2026, nine quantum computing firms split $2 billion in grants, with the government taking equity stakes in return. The administration’s growing use of equity stakes as a tool of industrial policy now spans nearly 20 companies across the semiconductor, critical minerals, and defense sectors.4 For hedge funds, government co-investment is a de-risking mechanism that makes private capital more comfortable. As a result, investments in high-tech, risky bets on newer technology suddenly become less risky if there is some form of sovereign participation, which, while modest in financial terms, creates an ‘insurance’ policy. Government participation also signals the administration’s and the state’s long-term thinking, providing a medium-term investable window for investors.

Semiconductors: Where Policy Meets Portfolio

Nowhere is the hedge fund pivot more visible than in semiconductors. Goldman Sachs Prime Brokerage data show that hedge funds have continued to rotate into Semiconductors & Semiconductor Equipment, with net exposure now at a five-year high.5 This is not purely a bet on AI demand. Rather, it is a bet that governments from Washington to Brussels to Tokyo will continue backstopping domestic chipmaking for national security reasons.

The thesis is reinforced by export controls and restrictions on outbound investment. The U.S. Outbound Investment Security Program (OISP), which took effect in January 2025, prohibits U.S. persons from investing in companies in specific geographies engaged in semiconductors, AI, and quantum technologies.6 The EU has followed suit, calling on member states to review outbound investments in semiconductors, AI, and quantum technologies. In effect, governments on both sides of the pond are drawing a map of where capital can and cannot go — and hedge funds are reading that map carefully.

Defense Manufacturing: Government Budgets as a Tailwind

In the wake of the conflict-ridden first decade of this century, global defense spending has become one of the most reliable structural tailwinds in the market. At a state level, this has led to ramifications. For instance, the U.S. administration has proposed a defense budget heading toward $1 trillion, with significant reconciliation funding layered on top of discretionary appropriations. In Europe, NATO-driven commitments have driven allied nations to rebuild and expand their defense-industrial bases. Nationalistic rhetoric has also pushed countries into focusing on defense spending as a hygiene factor. Global political alliances are redrawing the economics of defense production. The primary driver is the singular shift of focus from efficiency to security. From Europe to Japan, defense spending is undergoing a major overhaul, providing a long-term investment window to the investors.

Defense and energy equities have emerged as critical tools for portfolio risk mitigation in a geopolitical environment shaped by the Ukraine-Russia conflict and U.S. diplomatic interventions. Defense ETFs have expanded to include European and Asian players, recognizing that the rearmament cycle is not solely a U.S. story.

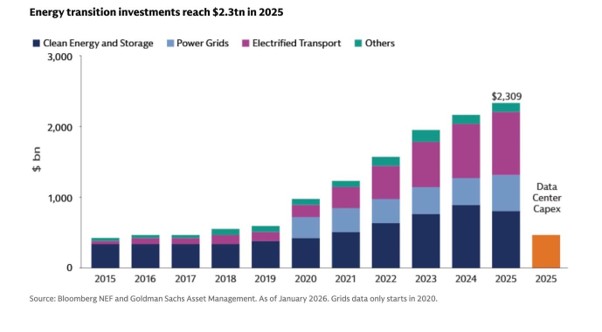

Energy Security: The $2.3 Trillion Structural Theme

The third vector that has emerged from the ‘new regime’ has been the transition of the energy narrative from a climate story to an energy security story — a shift that has considerably expanded its investable universe.

Source: Goldman Sachs Asset Management7

The energy transition is one of the largest structural investment themes of the decade, with global spending hitting $2.3 trillion in 2025, over five times global datacenter capex. Crucially, this spending extends well beyond renewables: grid modernization, electrified transport, storage, and clean industrial processes are all part of a buildout that governments are actively funding.

Government-backed initiatives in the U.S., EU, and elsewhere are channeling capital toward alternative refining capacity for critical metals, opening investable pathways for other producers to scale. For hedge funds, the recommended portfolio approach involves tilting toward Materials and Energy for raw-supply exposure, adding targeted Industrials and Chemicals for processing and domestic-supply resilience, and using IT and semiconductor names for the infrastructure layer that monetizes those inputs.

Strategic Supply Chains: The Critical Minerals Play

Perhaps the least understood — but potentially most lucrative — dimension of sovereign industrial policy is the scramble for critical minerals. Rare earths, lithium, cobalt, and other materials essential to semiconductors, EV batteries, and defense systems have become explicit targets of national strategy. A landmark July 2025 agreement between MP Materials and the Department of Defense to build a domestic rare earth magnet supply chain paired government ownership with offtake agreements, price floors, profit-sharing mechanisms, and concessional lending — a structure that effectively socializes downside risk while preserving upside for private co-investors.8

This model is increasingly the template. Hedge funds that understand how to position alongside government offtake structures and guaranteed revenue floors can access commodity-linked equity with substantially reduced volatility.

The Macro Framework: Controlled Disorder

Amundi’s Hedge Fund Investor Barometer captures the broader context well. The global economy is adapting to a new regime of “controlled disorder,” where AI-driven capex, industrial policy shifts, and supply chain reshoring sustain activity while inflation remains a structural theme.9 This environment rewards funds with the analytical capacity to track policy signals alongside financial fundamentals.

The old framework — where hedge funds mostly ignored the state as an actor — is no longer adequate. Today, the most sophisticated portfolios are mapping government industrial strategies the way they once mapped central bank policy cycles. The governments of the world’s largest economies have become the most consequential capital allocators of this decade. Hedge funds that understand this are not just adapting to a new world. They are being paid handsomely to navigate it.

Sovereign industrial policy is displacing austerity, and equity risk premiums are adjusting accordingly. Hedge funds, recognizing that government-backed stocks now offer structural advantages, are rewriting their investment frameworks.

For investors, the message is clear: policy is now a primary alpha driver. Success in the next decade will depend on identifying companies aligned with sovereign strategic priorities in semiconductors, energy security, defense, and critical supply chains.

Sources:

1. https://am.gs.com/en-us/advisors/insights/article/market-know-how

2. Ibid.

3. https://www.semiconductors.org/chip-supply-chain-investments/

5. https://am.gs.com/en-us/advisors/insights/article/market-know-how

7. https://am.gs.com/en-us/advisors/insights/article/market-know-how

9. https://research-center.amundi.com/article/2026-hedge-fund-investor-barometer