Higher-for-Longer Regimes and Corporate Debt Refinancing Risk

June 25, 2026

In the wake of the 2008 GFC turmoil, the corporate world entered a financial regime marked by ultra-low interest rates and quantitative easing (QE). Seizing the moment, corporations globally issued an unprecedented volume of long-term, fixed-rate bonds at historically low coupons to the extent that investment-grade and high-yield issuers alike termed out their balance sheets at coupons that, in hindsight, look almost quaint.

The Times They Are A-Changin’

The world is undergoing a dramatic shift, marked by geopolitical realignments, technology disruptions, and above all, an economic narrative defined by nationalistic economics. In a world where efficiency is being replaced by security as a prime driver of economic policy, the financial rules are also being rewritten. For instance, in the east, Japan, which had introduced and sustained ZIRP, has raised its interest rates three times in the last 18 months and is expected to hike again by December this year. In the US, despite a regime change at the Federal Reserve, the new chairman supported a hold, and traders are betting on an interest hike by December.

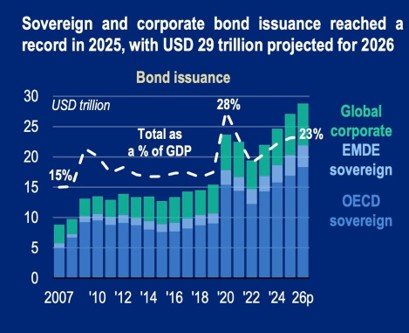

As the calendar advances through 2026, the corporate sector faces a critical reckoning: the multi-trillion-dollar “maturity wall.” A massive volume of cheap debt issued in the late 2010s and the early pandemic era is coming due, forcing companies to refinance at vastly higher prevailing interest rates. Evaluating this refinancing risk reveals profound implications for corporate balance sheets, capital deployment, and broader macroeconomic stability. Data from the OECD Global Debt Report 2026 highlights that total outstanding global corporate debt stood at a staggering $59.5 trillion by the end of 2025.1

Source: OECD Global Debt Report 20262

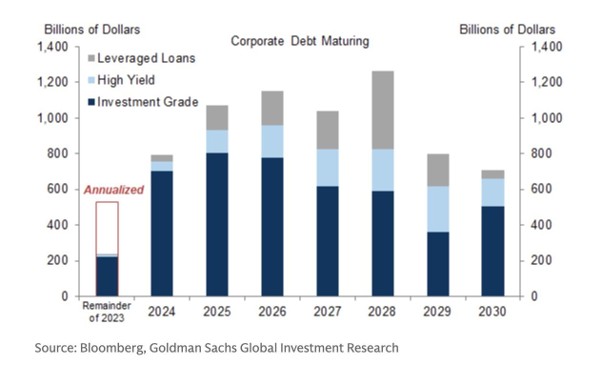

Corporate Debt Maturity Over The Next 5 Years

According to Goldman Sachs Research, from 2026 to 2028, roughly around a trillion dollars of corporate debt will mature annually. These are a combination of investment-grade debt, high-yield debt, and leveraged loans. From 2026, the share of investment-grade debt will gradually decrease through 2029, while the share of leveraged loans will rise correspondingly. Firms that locked in coupon rates between 2% and 4% in 2018 or 2020 are now stepping into a market where investment-grade yields hover much higher, and high-yield, speculative-grade issuers face coupons that could easily double or triple their existing financing costs.3

Source: Goldman Sachs Research4

Investment-grade debt is typically issued by large, cash-rich corporations and remains highly resilient. According to the OECD report, corporate credit spreads have remained historically tight due to robust aggregate earnings. Furthermore, sectors capitalizing on the expansion of artificial intelligence are attracting substantial external funding with relatively manageable stress. The real danger is at the lower end of the credit spectrum, where the global maturity wall for high-yield issuers has expanded aggressively, with peak refinancing obligations looming through 2026–2028.

The Capex and Employment Squeeze

When a firm is forced to absorb a massive increase in its interest burden, the macroeconomic fallout is felt directly through two key drivers of economic growth: capital expenditure (Capex) and payrolls. The Goldman Sachs report, using firm-level data from 1965, estimated that for each additional dollar of interest expense, firms tend to lower their capex by 10 cents and labor costs by 20 cents in 2025. Translated into job numbers, the estimated drag was small in any single month but cumulative and persistent: a few thousand fewer payrolls added per month, compounding over the refinancing cycle.

Consequently, the maturity wall serves as a delayed-transmission mechanism for monetary policy. Even if consumer spending remains stable, an aggregate pull-back in business investment and hiring can induce a synchronized slowdown across advanced economies. The firms most exposed to this dynamic are disproportionately unprofitable ones, which tend to cut capex and employment hardest when margin pressure rises — and the exit rate of such firms has stayed unusually low since the pandemic, meaning more zombie-adjacent balance sheets are still around to feel the squeeze.

Where The Stress is Actually Showing Up

Moody’s defaults data through early 2026 suggests the wall hasn’t triggered a crisis, but it has kept credit risk elevated and unevenly distributed. As of March 2026, the average one-year expected default probability for US-listed companies stood at 7.9%, down from 9.1% a year earlier but still elevated historically, while high-yield default probabilities sat at 3.2% — within the same range that has prevailed since 2023.5

Source: Moody’s6

Crucially, the rate outlook itself has hardened against borrowers: markets have sharply reduced expectations for Fed rate cuts in 2026, reinforcing a higher-for-longer regime that disproportionately hits floating-rate borrowers and near-term refinancers — a profile far more common in private credit portfolios than in public markets. That’s a meaningful bifurcation: companies with public bond access and staggered maturities have had room to manage the transition, while private-credit borrowers with floating coupons and concentrated maturities are absorbing the brunt.

Moody’s baseline forecast also places GDP growth around just 1.5%, barely above the “stall speed” below which defaults tend to accelerate, leaving little cushion if growth disappoints even modestly while the wall is still being climbed.

So What’s The Endgame?

The maturity wall isn’t a single cliff edge; it’s a multi-year repricing event that quietly raises the economy-wide cost of capital, firm by firm, as each cohort of 2010s-era debt rolls over. The macro drag — on capex, on hiring, on credit spreads — will likely keep showing up less as a dramatic shock and more as a persistent headwind, with the sharpest pain concentrated among weaker, more leveraged, and floating-rate borrowers who don’t have the luxury of waiting out the cycle.

In this higher-for-longer environment, scaling the maturity wall will require precise financial engineering from corporate treasurers and vigilant monitoring by central banks.

While strong aggregate corporate cash cushions and tight credit spreads suggest a systemic crisis is avoidable, the microeconomic reality will be restrictive. The inescapable reality of higher refinancing costs ensures that corporate cash will increasingly service past debts rather than fund future innovations, acting as a persistent drag on macroeconomic growth for the remainder of the decade.

Sources:

2. Ibid.

4. Ibid.

5. https://www.moodys.com/web/en/us/insights/data-stories/us-corporate-default-risk-in-2026.html

6. Ibid.