News Digest: Factors Influencing REIT Returns – Size No Bar

August 25, 2025

Real Estate Investment Trusts (REITs) represent a $1.5 trillion asset class, providing investors with liquid, regulated access to commercial real estate alongside steady income streams. A May 2025 study, REIT Factors by Letdin, Seagraves, and Sirmans, examined six REIT-specific return drivers – size, value, momentum, quality, low volatility, and short-term reversal – using data from 364 REITs between 1987 and 2023.

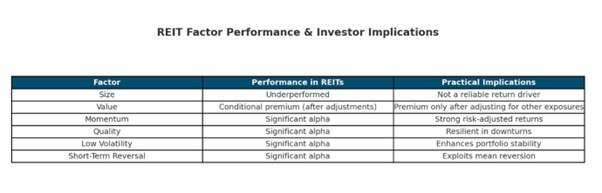

The research found that these REIT factors significantly outperform general equity models, raising explanatory power by 33% and cutting unexplained alphas by nearly 3% annually. Momentum, quality, low volatility, and short-term reversal were the most consistent alpha sources, while size underperformed and value only showed premiums after adjusting for negative exposures to other factors. Importantly, these anomalies proved distinct from traditional equity markets, underscoring the uniqueness of the drivers of REIT returns.

Performance varied across regimes: value suffered in crises like 2008–09 and 2020, whereas momentum and quality held up. Transaction costs were reduced, but did not eliminate factor profitability, making multifactor approaches both practical and resilient.

For investors, the key takeaway is that REIT-specific factors matter. Incorporating them into multifactor portfolios alongside traditional stock factors can reduce volatility, enhance diversification, and improve risk-adjusted returns, highlighting REITs’ distinct role in modern portfolio construction.

End Notes