Portable Alpha and SMAs: The New Efficiency Frontier for Institutional Portfolios

March 13, 2026

As we navigate the opening quarters of 2026, the institutional investment landscape is defined by a striking paradox: global liquidity remains abundant, yet the traditional engines of excess return, simple market beta, and private equity, are stalling under the weight of lofty valuations and “policy fatigue.” Institutional investors increasingly confront a structural reality: alpha within traditional long-only portfolios has become scarce, correlations across asset classes have risen, and liquidity constraints have become more pronounced.

Against this backdrop, a growing number of pensions, sovereign wealth funds, and endowments are revisiting a powerful idea first popularized two decades ago-portable alpha-and combining it with Separately Managed Accounts (SMAs) to create a more capital-efficient portfolio architecture. The result is what many asset managers describe as a new efficiency frontier for institutional portfolios.

Defining Portable Alpha

At its core, a portable alpha strategy aims to generate returns that exceed a specific market index, such as the S&P 500 or the Bloomberg U.S. Aggregate Bond Index. These strategies are built on two distinct pillars:

- The Beta Component: This represents the target index exposure.

- The Alpha Component: This is a separate source of excess return opportunities.

The power of this approach lies in effectively separating the target index’s returns (beta) from those of an alpha-seeking manager. This separation allows the manager’s alpha to be “ported” directly onto the investor’s chosen market index exposure.

The 2026 Alpha-Beta Mismatch

The primary challenge for today’s pension funds and sovereign wealth funds is “alpha-beta mismatch.” In a world where the S&P 500 recently flirted with its third consecutive year of 20%+ returns (a feat rarely seen since the late 1990s), investors are rightfully wary of a “beta cliff”. A “beta cliff” is a scenario where a fund’s returns, which previously seemed uncorrelated with the market, suddenly drop sharply in lockstep with the broader market due to hidden, high market exposure (beta).

Portable alpha solves this by decoupling the two components:

- The Beta: Replicated efficiently through low-cost derivatives (futures or swaps).

- The Alpha: Generated by an uncorrelated, high-conviction manager.

A key advantage of a portable alpha framework is that it allows investors to separate a portfolio’s active risk budget from its core beta allocation without disrupting the underlying market exposure. By doing so, it frees up capital that can be redeployed toward strategies designed to generate excess returns in areas of global markets where alpha opportunities may be more abundant. In practice, constructing the optimal portfolio allocation for market exposure (beta) is a very different exercise from allocating capital to strategies that aim to deliver excess returns (alpha). Portable alpha enables institutions to manage these two objectives independently, improving overall portfolio efficiency. By using derivatives to gain market exposure, investors “unlock” the underlying cash, which can then be “ported” into alpha-seeking strategies, often Equity Market Neutral, Global Macro, or Quant Multi-Strategy, that aim to outperform the financing cost of the derivatives.

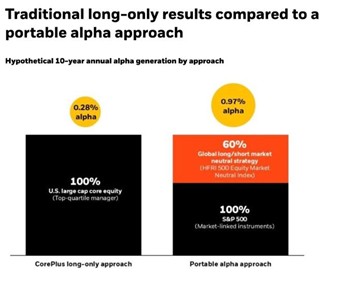

Source: BlackRockSource1

The above is a hypothetical illustration provided by BlackRock of how a portable alpha approach works. This represents model-driven allocations, as depicted above, to the underlying top-quartile (25th percentile) managers in the eVestment Large Cap Core category as of September 30, 2024. The average top quartile manager delivered 0.28% alpha (net) after all fees and expenses have been deducted. In a portable alpha approach, a manager delivered 0.97% alpha (net) after all fees and expenses had been deducted.

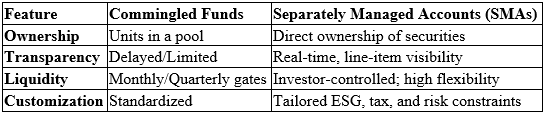

SMAs: The Engine of Customization

While portable alpha is the strategy, the Separately Managed Account (SMA) is the vehicle, making it viable in 2026. Unlike commingled funds, where an investor is one of many in a pooled “black box,” an SMA offers direct ownership of the underlying securities and a bespoke mandate.

For institutional giants, the appeal of SMAs in a portable alpha context lies in treasury efficiency. According to BNP Paribas, treasury efficiency was the most cited reason for the 61% surge in SMA capital allocations between 2023 and 2025.2 SMAs enable better collateral management, allowing investors to optimize the cash and margin required to support the “ported” beta.

Hunting for the “Elusive” Return

In 2026, alpha is not just harder to find; it is more idiosyncratic. We are seeing a shift from “thematic” investing toward “security selection” driven by market dispersion.

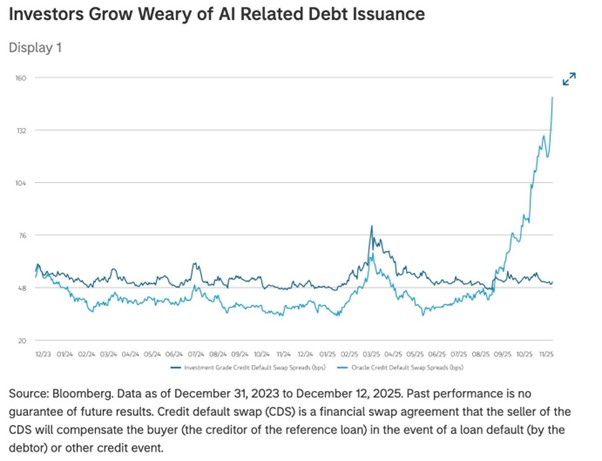

- The AI Nexus: While the AI boom continues, signs of “creative destruction” are appearing. According to Morgan Stanley, this creative destruction will follow signs of excess: where “vast amounts of capital have been spent funding a to-be-determined amount of future revenue”.3Institutional investors are using SMAs to short specific AI “laggards” while maintaining long beta exposure to the broader tech sector. The primary example they cite is Oracle, where the Credit Default Swap spread has far exceeded the average investment-grade CDS spread, raising concerns about Oracle’s ability to realise those revenues and/or service the debt.

Source: Morgan Stanley4

- Geopolitical Resilience: With the global order splintering into competing trade blocs, “Global Macro” strategies have become a favorite source of alpha. SMAs allow sovereign wealth funds to implement these strategies with specific regional exclusions or inclusions that match their geopolitical risk profiles.5

Navigating the Risks

This efficiency frontier is not without its thorns. The success of a portable alpha strategy in an SMA hinges on three critical factors:

- Financing Costs: As central banks maintain a “higher-for-longer” or volatile rate environment, the cost of the swaps and futures used for beta must be meticulously managed.

- Manager Skill: If the alpha manager underperforms the cash financing rate, the “portable” component becomes a drag on the total portfolio.

- Operational Complexity: SMAs require more robust back-office support than traditional funds. However, the rise of agentic AI models in 2026 is helping LPs automate much of this administrative burden.6 This ranges from analyzing sector dynamics, evaluating model implications, and assessing potential risk factors to support investment decision-making.

The Future is Bespoke

The era of “set it and forget it” institutional allocation is over. By 2026, the frontier of efficiency is defined by control. The combination of portable alpha and SMAs allows institutions to remain fully invested in the market while pivoting their active risk budget toward the most fertile alpha ground.

As liquidity becomes a premium and market dispersion increases, this structural evolution ensures that the largest portfolios on earth can move with the agility of a boutique shop, without sacrificing the scale of a titan.

The Next Generation of Portable Alpha

The evolution of portable alpha continues. Today’s implementations increasingly incorporate diversified sources of alpha, including:

- Systematic macro and managed futures

- Alternative credit and private lending

- Market-neutral equity strategies

- Quantitative factor portfolios

Some managers are even extending the framework into “return stacking” strategies that combine multiple alpha streams alongside core beta exposure.

For example, alternative credit hedge funds have recently been positioned as attractive sources of alpha within portable alpha frameworks because they can deliver stable returns with low correlation to public markets.7

This diversification is crucial because portable alpha succeeds only when alpha sources are truly independent of the underlying beta exposure.

Sources:

1. https://www.blackrock.com/institutions/en-au/insights/investment-actions/portable-alpha-strategies

2. https://usa.bnpparibas/en/bnp-paribas-publishes-results-of-its-2026-hedge-fund-outlook/

4.Ibid.

5.https://www.jpmorgan.com/content/dam/jpmorgan/documents/wealth-management/outlook-2026.pdf

7.https://www.fasanara.com/insights/posts/portablealpha