Private Credit: Separating the Noise from the Signal

April 29, 2026

The headlines have been alarming. Several of the world’s largest private credit funds – Blackstone, BlackRock, Blue Owl, Morgan Stanley, Apollo – moved in early 2026 to restrict investor redemptions. Fund managers who had positioned their products as “semi-liquid” suddenly appeared anything but. Most investors already know the broad strokes of what happened. The more important question is: why is the situation now as bad as it looks, and what does it mean for private market investors going forward?

Why the Negative News Now?

The gating episode did not come out of nowhere: it was the culmination of several slow-burning dynamics colliding at once.

The private equity liquidity drought. Private equity has been generating historically low distributions since 2022. Annual distribution rates for LP investors have fallen from roughly 20% to around 10%, according to research1 from Allianz. With IPO markets still largely closed and M&A activity concentrated among mega-cap deals, GPs have been unable to return capital at the pace investors expected. This has created compounding pressure: LPs who are not receiving distributions from PE funds are simultaneously more reluctant to recommit capital and more eager to reduce illiquid exposure elsewhere, including private credit. The private credit redemption wave is, in part, a downstream consequence of the frozen PE exit environment.

The private equity secondaries pressure valve. As PE distributions dried up, secondaries emerged as the release valve. Secondary market volume approached $200 billion in 2025, and GP-led transactions now represent close to 45%, according to market estimates.2 This surge in secondary activity has compressed discounts and eroded the liquidity and complexity premiums that historically made secondaries so attractive. As one analysis by UBP noted, a tool designed to mitigate structural constraints is now reshaping the economics of secondaries. This dynamic has left some LPs feeling that all liquidity paths – PE secondaries, credit secondaries, redemption windows – are narrowing simultaneously.

The retail investor is under stress. Between 2021 and 2025, private credit managers raised $1.3 trillion in new capital globally, much of it through semi-liquid evergreen funds marketed to high-net-worth individuals and family offices. These investors came in seeking yield – at the peak, all-in yields exceeded 11%. As rates declined, those yields normalized toward 8.5%. Simultaneously, a series of high-profile events, ranging from bankruptcy filings and NAV write-downs to an aborted Blue Owl fund merger, rattled retail investors who had never experienced a private credit stress event before. The redemption surge was, in significant part, a crisis of confidence among newer, less experienced investors, not a fundamental judgment about the asset class.

Is It Only a Narrow Part of Private Credit That’s Stressed?

This is arguably the most important question. The answer is yes, the stress is concentrated, not systemic.

The problems are overwhelmingly concentrated in two places: large-cap, software-heavy direct lending and retail semi-liquid BDC structures. Private credit is a broad umbrella. As an AIMA report points out, direct corporate lending accounts for only about half of the $3 trillion private credit universe.3 The rest encompasses infrastructure debt, commercial real estate debt, asset-based finance, insurance-linked strategies, and other areas that have not been meaningfully affected by the current stress.

Even within direct lending, the data suggests the problems are concentrated among specific fund types and borrower segments. A report by Proskauer, which tracked senior-secured and unitranche loans across 691 loans representing $144.5 billion in principal, suggested a default rate of just 2.46% in Q4 2025, with Proskauer partners describing “stability and resilience” in the broader picture.4

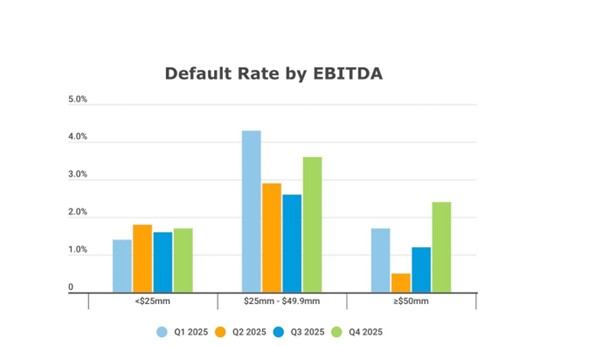

Source: Proskauer5

The AIMA 2025 survey of flagship corporate lending funds showed an average non-accrual rate of just 2.2%.6 Meanwhile, BDC data showed all-in yields still at 9.76% after 150 basis points of rate cuts, with trailing one-year realized losses of only 0.66%, figures that do not describe a sector in crisis. J.P. Morgan’s Private Bank, in its March 2026 analysis, made the important point that gating mechanisms “are prudent tools” and that it is “entirely plausible” for some non-traded BDCs to gate without this being an indicator of credit stress, but rather a structural feature of those vehicles.7

The nuance that matters: Fitch’s Privately Monitored Ratings portfolio – which skews toward smaller, more opaque borrowers – recorded a 9.2% default rate. But these are not the institutional-grade, middle-market loans that dominate most allocators’ portfolios.8 Companies with EBITDA below $25 million are experiencing the most strain; larger, better-sponsored borrowers with EBITDA above $50 million saw default rates of just 1.44% in 2025. The stress is real, but it is segmented.

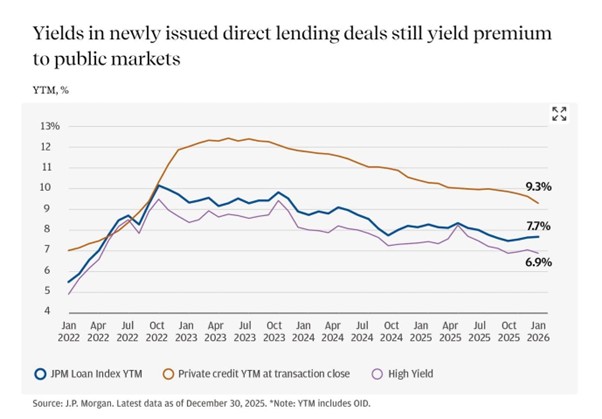

Despite all the misgivings, JP Morgan reports that yields to maturity in newly issued direct lending deals have remained above comparable public market yields since early 2022, with a noticeable peak in 2023 followed by a gradual decline into 2025.9 Private credit yields at transaction close are the highest of the three series, and most of the period sit around 10–12% at the 2023 peak before easing to about 9.3% by late 2025.

Source: JP Morgan Private Bank10

Are There Visible Defaults Happening?

Yes! However, the picture is more nuanced than the headlines suggest. The most notable actual defaults have been Tricolor Holdings (a subprime auto lender) and First Brands Group (an auto parts company) in late 2025, made famous by Jamie Dimon’s cockroach analogy.11 Beyond these, a report from Yahoo Finance reveals that distressed exchanges – where borrowers restructure loans to defer interest rather than make hard payment defaults – now account for 94% of credit downgrades.12 This “amend and extend” behavior obscures real stress that is not yet crystallized into outright losses.

The shadow default rate, where companies use payment-in-kind (PIK) structures to defer cash interest, has more than doubled from 2.5% in 2021 to 6.4% by Q4 2025, according to Lincoln International.13 PIK usage across BDCs now accounts for roughly 8% of average investment income. These are warning signs, not yet realized losses, but they represent loans that are carrying deferred risk.

Despite the noise generated by “Saaspocalypse”, technology software, notably, recorded only three unique defaults in the 12 months through January 2026, with a default rate of just 1.9% – far below the alarm implied by the AI disruption narrative. As Fitch noted, “the mission-critical nature and high switching costs of many enterprise software products continue to protect incumbent operators.”14 The rapid progression of Generative AI began disrupting traditional software business models, leading to a “Saaspocalypse” and rising defaults in the mid-market space. The AI disruption risk is real over the medium term, but acute defaults in SaaS lending have not yet materialized at scale.

What Is the Impact on Other Private Market Strategies?

Here is where investors should take genuine comfort.

Infrastructure debt remains one of the most insulated strategies. Many infrastructure projects benefit from inflation-linked revenues and regulated frameworks. The demand for capital, in data centers, energy transition, transportation, and utilities, is structural and independent of corporate credit cycles. Since these are high-capex, driven by sovereign policies, and in many cases backed by sovereign intent, infrastructure debt combines yield stability with downside protection, making it particularly valuable in the current environment.

Insurance-linked securities (ILS) are performing their role as an uncorrelated return stream. ILS performance is driven by insured event outcomes, not economic growth or corporate credit quality. Current valuations remain attractive, with limited loss activity in recent years enabling meaningful repricing. Despite compressed spreads driven by increased demand for uncorrelated income, the fundamental case for ILS as a stabilizing force in a credit-stressed environment remains intact.

Commercial real estate debt has, in many respects, already been through its stress cycle. The 2022–2024 repricing of real estate values, particularly in office, means that investors entering CRE debt today do so at a lower basis with more realistic underwriting assumptions. Interestingly, the reset that private credit direct lending is only beginning to experience has already occurred in real estate credit.

Life Settlements represent a sophisticated investment strategy powered by actuarial precision rather than market sentiment. Unlike traditional private assets, which fluctuate with corporate credit cycles, Life Settlements remain structurally uncorrelated with economic stress. They offer a rare level of security within the Private Assets class, providing investors with a robust profile that carries virtually zero counterparty risk.

Asset-based finance (ABF) is increasingly seen as the next chapter of private credit growth. Unlike direct lending, ABF is underwritten against hard collateral – homes, cars, receivables, aircraft – rather than corporate cash flows. The collateral-backed nature of these strategies provides a fundamentally different risk profile, and multiple major managers are pivoting capital toward ABF as a direct response to headwinds in direct lending.

And Now?

The current environment is the first genuine stress test for private credit as a mainstream asset class. It reveals real structural weaknesses across several situations, ranging from semi-liquid retail structures to software-laden portfolios underwritten at peak multiples, and the illusion that quarterly liquidity windows can reliably coexist with multi-year loan books. Those weaknesses deserve scrutiny.

But here is the real McCoy: the stress test is also doing what stress tests are supposed to do: separating well-structured, appropriately managed strategies from those that grew too fast, too concentrated, and with too little regard for the mismatch between investor expectations and underlying asset liquidity.

For allocators, the roadmap is relatively clear. First, understand the vehicle, not just the asset class — closed-end, institutional-grade structures with experienced managers have a fundamentally different risk profile than retail BDC windows.

Second, diversify within private credit — the case for infrastructure debt, ILS, ABF, and CRE debt is arguably stronger today than it was twelve months ago, precisely because capital is rotating away from direct lending.

Third, recognize that the yield compression in direct lending is not going to reverse quickly — all-in yields have moved from 11%+ to 8.5%, and that recalibration may prompt a broader reassessment of what private credit is meant to do in a portfolio.

And fourth, view the current dislocation as a vintage opportunity: as most mega-fund managers have noted, the managers with the discipline to walk away from bad deals during the boom years are now the ones positioned to deploy into a reset market.

Private credit is not broken. The credit cycle has not been repealed — it was merely deferred. The asset class is growing, and the growing pains are visible. That is not the same thing as a crisis.

And no, private credit is not a checking account. Not today, not tomorrow.

Sources:

2. https://www.dcadvisory.com/media/2jwpve1y/global-secondary-market-report-2025.pdf

3. https://www.aima.org/compass/insights/private-credit/financing-the-economy-2025.html

5.Ibid.

6. https://www.aima.org/compass/insights/private-credit/financing-the-economy-2025.html

10. Ibid.

11. https://finance.yahoo.com/news/jamie-dimon-warned-cockroaches-now-023108446.html