Real Estate, REITs & Geopolitics: How Infrastructure, Supply Chains and Trade Flows Reshape Real Estate Risk

November 10, 2025

Since the advent of the Industrial Revolution until the ‘noughties’ of the 21st century, the mantra for economic activity was defined by ‘efficiency’. Consequently, the Real Estate industry was marked by trade connectivity, cost efficiency, and stable capital flows – indicators of capital efficiency. Real estate growth was dictated purely by demographics, zoning laws, and interest rates. If the cost of production was lower halfway across the world and the logistics costs made it cheaper overall to shift production, so be it. At the end of the day, what mattered was the balance sheet.

Not that the balance sheet has become any less important, but the global landscape now has additional complexities built into the system – economic nationalism, local governance factors, and, most importantly, a shift away from efficiency to Security. It is no longer enough to be capital-efficient; it is also necessary to secure supply chains and insulate them from potential geopolitical disruptions. If anything, 2025 will go down in the history of the global mercantile system for legitimising the return of ethnocentricity to the international industrial environment. This transition – from hyperglobalization to localization, from efficiency to security, from apolitical economic dynamics to geopolitically-influenced landscape – is creating new risks and unprecedented opportunities for investors in physical assets, particularly within the industrial, logistics, and digital infrastructure sectors represented by Real Estate Investment Trusts (REITs).

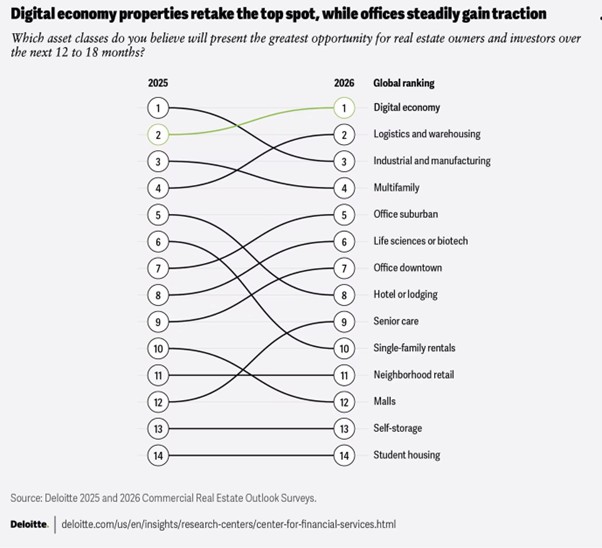

Source: Deloitte Insights1

For real estate investors and REIT honchos, geopolitical diversification is no longer a nice-to-have luxury – it’s a strategic necessity. A data center halfway across the world may be lucrative. Still, it may also carry exposure to diplomatic rethinks, attritional risk, or may simply constitute a trade barrier that was not there when it was conceived. caused by pandemics and conflicts have pushed corporations towards a complex set of dynamics in which globalization will co-exist with regionalization, or even outright “friend-shoring.” This is driving demand for new infrastructure, manufacturing zones, and logistics centers closer to end markets.

REITs have begun responding by diversifying both geographically and sectorally. Funds with exposure to essential infrastructure – fiber network topologies, LNG terminals infrastructure, logistics parks near emerging “China-plus-one” manufacturing zones – are seeing increased interest. Conversely, REITs concentrated in markets vulnerable to cross-border conflict have experienced valuation compression and higher risk premiums. This has immediate and visible consequences for industrial real estate. Companies are moving manufacturing closer to end consumers or to politically stable trade partners.

This strategic re-evaluation is fueling the rise of smaller, highly automated microfactories3 capable of achieving profitability at a fraction of the scale previously required. The goal is speed, customization, and supply chain redundancy, needs that a massive centralized and distant manufacturing plant will be unable to deliver.

REITs in an Age of Weaponized Capital

The most direct impact is felt in the vast industrial and logistics sector, the backbone of modern commerce. REITs focusing on this sector are now implicitly making a geopolitical bet. The winners will be those who prefer nearshoring and redundancy. Losers will include those highly dependent on long-distance, single-source trade corridors, particularly those facing geopolitical friction and older distribution centers that fail to integrate into the new, localized network, and will risk obsolescence. The property’s physical location is judged not just by access to highways, but also by access to a resilient, secure supply chain.

Additionally, even infrastructure-adjacent real estate is now a strategic battleground. Governments are scrutinizing ownership of key infrastructure – ports, telecoms, and industrial parks. The recent Nexperia incident4 is only a harbinger for things to come. Nations are reevaluating foreign direct investment in assets deemed “strategic,” raising transaction barriers or requiring security clearance.

The Rise of Digital Infrastructure as Geopolitical Real Estate

The digital economy is one of the major fronts of the geopolitical real estate revolution. As global AI investment accelerates, estimated to involve trillions of dollars in spending, the demand for computational power is immense. This necessitates a massive, ongoing buildout of physical data centers.

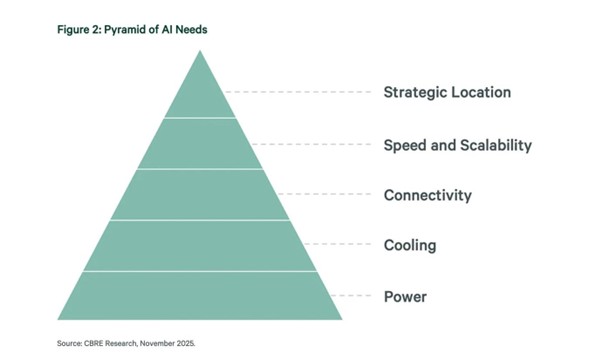

Source: CBRE Research5

Far from being expensive IT assets (server farms, packaging assemblies) built on a massive scale, data centers and chip manufacturing are being viewed as critical national infrastructure. The combination of data sovereignty laws (requiring data to be stored within national borders), the narrative around processing sovereignty, and the sheer utility requirements of AI and GPUs means that data center and processor manufacturing locations are increasingly strategic, both at a computational level and also at a societal level.

- REIT Opportunity: Digital infrastructure REITs, which own and operate these centers, are benefiting from the structural, long-term demand for secure, high-power-density facilities. The risk is shifting toward regulatory compliance and utility access, as data centers must now meet stringent security and sustainable power generation standards.

- Energy Nexus: This demand is fundamentally linking the energy grid to real estate. The availability of clean, reliable, and abundant power and water is now a key determinant of a data center property’s value and determines the location of a microprocessor assembly, making security of key utilities a new real estate risk factor.

For investors in global listed real estate – a sector that has historically demonstrated strong returns and diversification benefits – the investment process continues to evolve. The traditional method of allocating to broad global REIT indices is no longer sufficient. The successful portfolio today requires a granular, macro-driven approach that assesses four key risks:

- Trade Corridor Risk: Is the industrial property linked to a growing, protected trade bloc (e.g., North America, EU friend-shoring) or a vulnerable, long-distance corridor?

- Regulatory Risk: Does the property (especially office and residential) face rising taxes, protectionist measures, or stringent data localization rules?

- Inflationary Risk: Structural inflation driven by deglobalization means new construction costs are permanently higher, making existing, well-located, high-quality assets more valuable due to replacement costs.

- Utility Risk: Does the location have guaranteed, stable access to the clean power and water required for future digital and industrial tenants?

The Future Playbook: Scenario Modeling and Geopolitical Underwriting

Real estate firms and REITs with sophisticated geopolitical risk frameworks will likely outperform. This means integrating geopolitical scenario planning into underwriting, stress testing supply chain nodes, and embedding resiliency into asset selection.

The winners will be those who foresee where trade corridors, production networks, and political incentives converge. Today, that means tracking developments from India’s industrial corridors and the Middle East’s logistics boom, to U.S.-backed semiconductor ecosystems and LATAM’s manufacturing resurgence. For REITs, the future will belong to those who can stack yield with strategic foresight and build portfolios that withstand not just market cycles but the tectonic shifts in global power.

Sources:

2. https://www.jll.com/en-in/insights/market-outlook/global-real-estate

3. https://www.bain.com/insights/microfactories-the-back-to-local-moment/

4. https://www.therealestatecpa.com/blog/how-tariffs-impact-real-estate-investors-in-2025/

5. https://www.cbre.com/insights/briefs/ai-necessitates-new-blueprint-for-digital-infrastructure