The Art of Active Alpha: Mastering the Hedge Fund of Funds Approach

May 2, 2026

In a world crowded with passive strategies and index-hugging portfolios, actively managed Hedge Fund of Funds (FoFs) represent one of investing’s most demanding disciplines. They require not only the analytical rigor to identify exceptional managers but also the structural sophistication to build a portfolio that generates returns above what any single fund could deliver. At its core, an actively managed FoF is a dynamic, living organism — one that must be continuously monitored, stress-tested, and, when necessary, decisively restructured.

This is not a strategy for those who are passive at heart.

Why Alpha Matters — and Why It Matters Even More in FoFs

Alpha is the singular justification for active management. As a foundational principle, in a single-manager hedge fund, alpha generation is relatively straightforward to attribute: a skilled manager makes concentrated, high-conviction bets, and either they deliver, or they do not. In a Fund of Funds, the challenge compounds — you now have two layers of fees, two layers of decision-making, and two layers of potential alpha destruction.

This is precisely why alpha generation in FoFs is an existential issue, not just a characteristic. Research into FoF performance finds that persistent alpha is achievable in the cross-section of FoFs, but only for managers who actively manage exposures rather than holding a static basket of funds.1 The value proposition of an actively managed FoF is the construction of a portfolio of hedge funds that, in combination, delivers more than the sum of its parts: superior risk-adjusted returns, lower correlation to public markets, and exposures a single manager simply cannot provide.

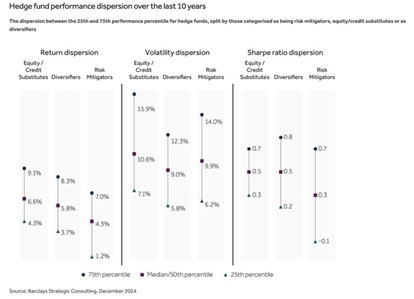

One of the strongest arguments for active FoF management is the sheer scale of performance dispersion in the hedge fund universe.

Source: Barclays Private Bank2

The return gap between a manager in the 75th percentile of performance and the 25th percentile is approximately 17 percentage points per year — a differential so large that passive allocation across the universe destroys value relative to skilled selection. This dispersion is even more pronounced in higher-volatility environments, meaning that the periods when markets are most turbulent are precisely when manager selection matters most and passive approaches fail hardest.

Taking an Active Approach: Beyond Manager Selection

Many FoFs pride themselves on rigorous due diligence — quantitative screening, qualitative interviews, operational reviews. But genuine active management extends far beyond the initial investment decision. It means actively managing exposures across the portfolio in real time. Elevated volatility, greater dispersion across sectors and individual securities, and higher interest rates have historically created conditions for active strategies to outperform traditional passive approaches — and Fund of Funds that can rotate toward the right strategy at the right time captures this advantage systematically.

Source: Resonanz Capital3

An actively managed FoF might, for instance, rotate from discretionary global macro funds during periods of low volatility into market-neutral equity strategies during high-dispersion environments.

Experienced allocators scale macro and CTA risk when policy regimes, rates, and FX trends experience breaks. These are not passive decisions baked into an annual strategic asset allocation. They are dynamic, conviction-driven calls made on a shorter time horizon, informed by both top-down macro analysis and bottom-up fund-level intelligence.

In short, active management in a Fund of Funds is not just about finding the right managers — it is about building the right portfolio at the right time and being willing to rebuild it when the time demands it.

To break down why that mindset matters:

- Manager Selection vs. Portfolio Construction:Finding five “star” managers is useless if they all have the same blind spots. The real skill is ensuring their strategies complement each other—for example, pairing a deep-value manager with a high-growth specialist so the portfolio doesn’t tilt too hard in one direction.

- The “Right Time” (Macro Awareness):A manager who crushed it during a period of low interest rates might struggle when inflation spikes. Active management means recognizing when the economic “weather” has changed and swapping out managers whose styles no longer suit the environment.

- The Willingness to Rebuild:This is the hardest part. It requires overcoming the “endowment effect”—the tendency to stick with a manager just because you’ve had a long relationship or they performed well three years ago.

Essentially, an effective FoF manager acts more like a sports GM than a scout. It’s not just about drafting the best players; it’s about making sure the roster works together and being brave enough to trade a veteran when the team needs a new direction

The Entry and Exit Imperative: Knowing When to Leave

Markets change. A strategy that generates consistent alpha in one regime can become a chronic underperformer when conditions shift. Once a manager grows beyond a certain threshold or becomes widely followed, capacity constraints and alpha decay set in — future results tend to disappoint as slippage increases and the edge erodes. Key person departures, style drift, and operational weaknesses are among the risks institutional investors monitor to assess whether a manager’s edge remains intact. An FoF that lacks both the conviction and the structural ability to redeem from underperforming funds is not actively managing anything.

The rigorous, clinical, and process-driven discipline of exit separates a genuinely active FoF from one that merely conducts periodic due diligence. Sophisticated allocators monitor peer correlation, factor loadings, and hit-rate decay.

Effective due diligence for alternative investments requires a multi-dimensional approach that balances potential upside with structural integrity. A robust evaluation centers on eight pillars: verifying return quality through skill-based alpha, stress-testing redemption liquidity, and ensuring strategic consistency across market cycles. Advanced risk intelligence must forecast tail risks, while operational audits verify the firm’s fiduciary architecture and governance. Furthermore, assessing downside insulation (or “airbag” mechanisms) and mandate alignment ensures the fund complements a broader portfolio without redundant exposure. By merging rigorous operational and strategic scrutiny with data-driven metrics, investors can convert complex qualitative observations into actionable insights, ensuring long-term fiscal vitality.

Liquidity: The Infrastructure of Active Management

None of the above — dynamic reallocation, timely exits, tactical positioning — is possible without the right liquidity architecture. Redemption liquidity is not a secondary consideration in a Fund of Hedge Funds. It is the foundation upon which every active decision rests.

Thoughtful FoF managers, therefore, construct their portfolios with liquidity tiering in mind. A portion of the portfolio is allocated to highly liquid, shorter lock-up strategies that can be redeemed quickly. A core allocation targets funds with quarterly liquidity — the workhorse layer. A smaller, deliberate allocation may accept annual or longer liquidity in exchange for access to less-crowded, higher-conviction strategies where the illiquidity premium is genuinely compensated. Research confirms that lower redemption frequencies, longer notice periods, and gate provisions are among the most effective structural protections available—but they must be calibrated to the FoF’s obligations to its end investors.4

The Edge of Active FoF Management

Actively managed Hedge Fund of Funds strategies, executed with discipline, offer something genuinely rare: access to diverse, uncorrelated sources of return across market environments, structured within a portfolio framework that is itself actively managed for alpha. Truly innovative managers with sustainable advantages should continue to generate alpha across changing market conditions, and the FoF that identifies such managers early, constructs exposures thoughtfully, manages liquidity with precision, and exits without hesitation when fundamentals change is adding real, measurable value.

Knowing when to enter a fund is only half the equation. True skill lies in knowing when to leave — and having the liquidity to do so. It demands intellectual honesty, operational discipline, and the courage to make uncomfortable decisions.

Sources:

4. https://thehedgefundjournal.com/redemption-terms/